When it comes to valuation, we are talking about how much something worth. Well, this premise itself is highly subjective, because in the end, how much a thing worth is really in the buyer’s eye. That is why many people say valuation is an art, not a science. More complicated calculations do not make valuation more concise. However, we need some methods to estimate the value of investment target, for at least these methods can be used as parameters to facilitate in making final decisions.

Valuation models assume that markets are inefficient but eventually the true value of a project will be discovered. The valuation methods used for mature business, startup or unprecedented projects can vary significantly. The less mature a target is, the more risks it will be involved, and the more estimations will be used in valuation. However, financial analysts’ valuations are biased, and it is always recommended to check the answer against common sense.

DCF Method

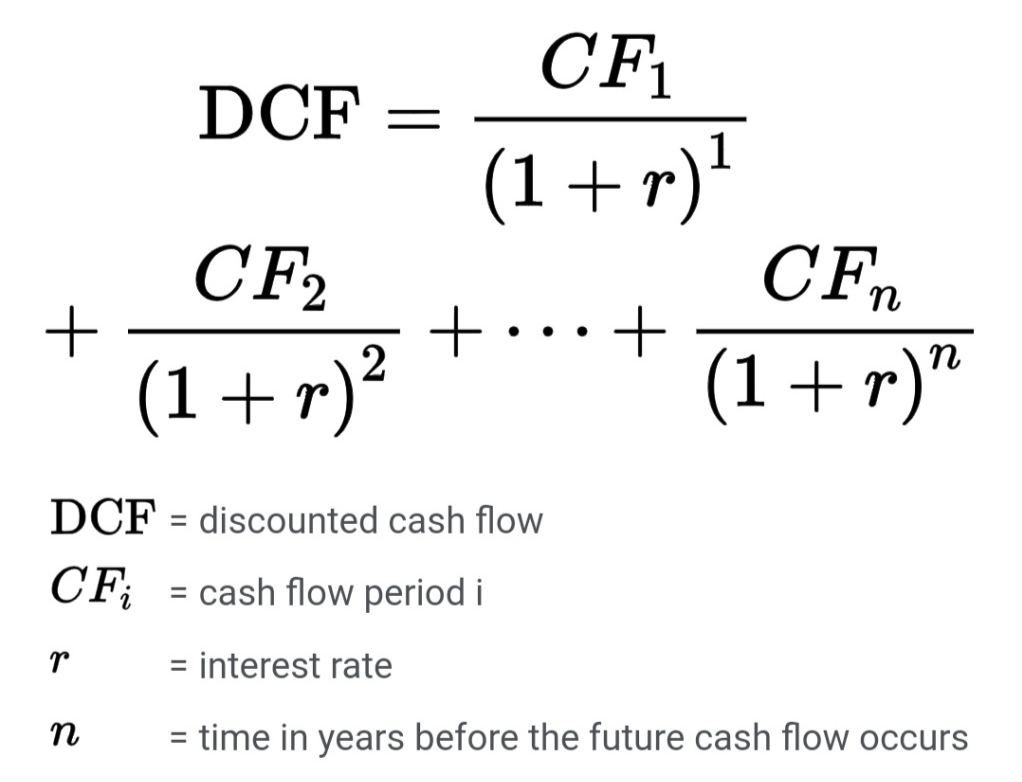

DCF represents Discounted Cash Flow. Well, apparently, this method is more useful to companies which have financial track records, because the results can be more predictable and justified based on historical performance. For startups without financial track records, this method can only be used as a reference (a sign of entrepreneurial confidence and commitment) in conjunction/comparison with other methods.

Principles of DCF

- Assumes that the project/firm has intrinsic value based on its current cash flows, and the growth in and risk of those cash flows.

- The following will be estimated:

- Effective life of the project/firm

- Expected cash flows-properly timed over the effective life, and

- The right discount rate

DCF analysis is the basis of the most popular project valuation methods. There are a few elements in the DCF model:

We can see from the model, The accumulated discounted future cash flows. Usually for valuation, the time span is 5 or 6 years. Proper estimation of Discount factor is also very important, as discount factor is applied based on the fundamental concept in finance, the time value of money-that a dollar today will be more valuable that a dollar received in the future (time preference, inflation, future uncertainty). Thus when using DCF method, both future cash flow calculation and the discount factor used can be quite tactical/ “tricky”, which involves lots of computational work.

- Calculating the Discount factor

There are different ways to calculate the discount factor, we may often see the following are commonly used: Internal Rate of Return (IRR), Weighted Average Cost of Capital (WACC) and Capital Asset Pricing Model(CAPM).

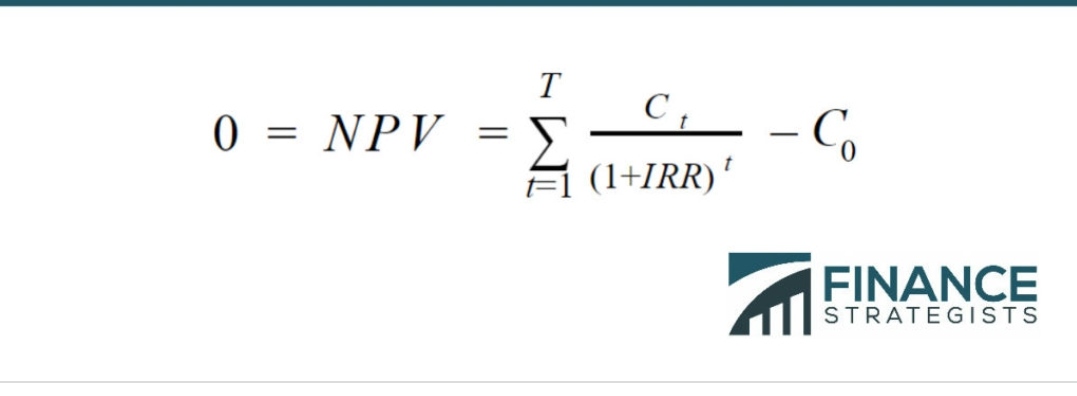

1)IRR technique

A project’s Internal Rate of Return (IRR) is simply the discount rate that when applied to a project’s expected cash flows yields NPV = 0.

Projects are accepted if IRR > Cost of capital. However, when applying IRR technique, Caution needs to be exercised, because in the following cases, IRR is not recommended or not enough to use alone:

- Some projects don’t have IRR, so this technique is only guaranteed to work if all the negative cash flows occur before positive cash flows. (Equity financing v.s. Debt financing).

- Project can have multiple IRR, for example, Cash inflow in the beginning of the project and cash out flow in the end of the project.

- For mutually exclusive projects, we might get inconsistent rankings which is conflicting with NPV calculation, so it is not that simple to simple compare project’s with IRR, it is always recommended to double check with NPV.

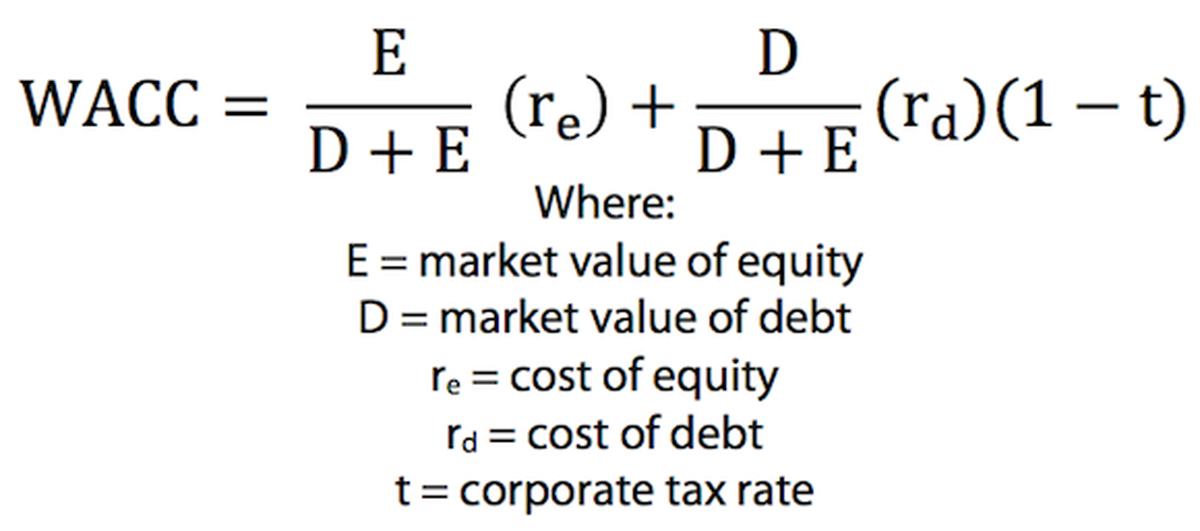

2)WACC

The weighted average cost of capital (WACC) is a calculation of a firm’s cost of capital in which each category of capital is proportionately weighted. Thus WACC is the discount rate for entire company which compose of cost of debt Kdand also cost of equity Ke.

t is the corporate tax rate, and V is Current market value of debt and equity (not book values!). However, WACC can be quite difficult to estimate from outsiders of a firm.

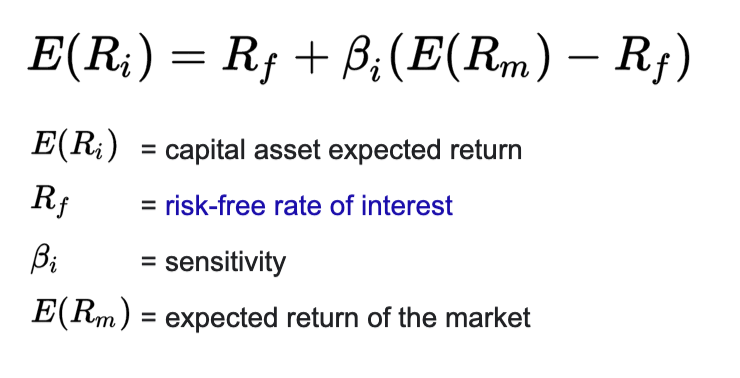

3)CAPM

The capital asset pricing model was developed by the financial economist William Sharpe, set out in his 1970 book Portfolio Theory and Capital Markets. It provides estimates of a project specific discount rate for a given level of systematic risk that can not be diversified.

Rf is risk-free rate which can be referenced from government bonds and treasury bills. The second half of right hand of the equation is the adjustment for risk indicated by beta. The difference between E(RM) and Rf is called Market risk premium, which can be found in online resources as parameters for calculation(usually from 5%-8%). However, It is a forward looking model of expectations. When graph CAMP, we end up with the security market line (SML).

| Advantages about DCF | Disadvantages about DCF |

Forward looking-better aligned with wealth creation Focuses on the business operations (Somewhat) removed from market irrationalities. | Makes many assumptions Computationally intensive-information is not always reliable and is always noisy Depend crucially on growth and risk assessment There is no guarantee that the market value(price) will quickly reflect the DCF value. |

Firms tend to use firm-wide discount rate WACC rather than project specific discount rate CAPM. Since WACC tends to neglect systematic risk-beta, when keep assessing projects with WACC, big companies’ systematic risk tent to increase because more riskier projects were accepted because of higher WACC even though those projects might indicate negative NPV, which would gradually lead to the decline of firm value. For smaller firms, such issue is less likely than bigger firms because they are likely operating in more focused areas.

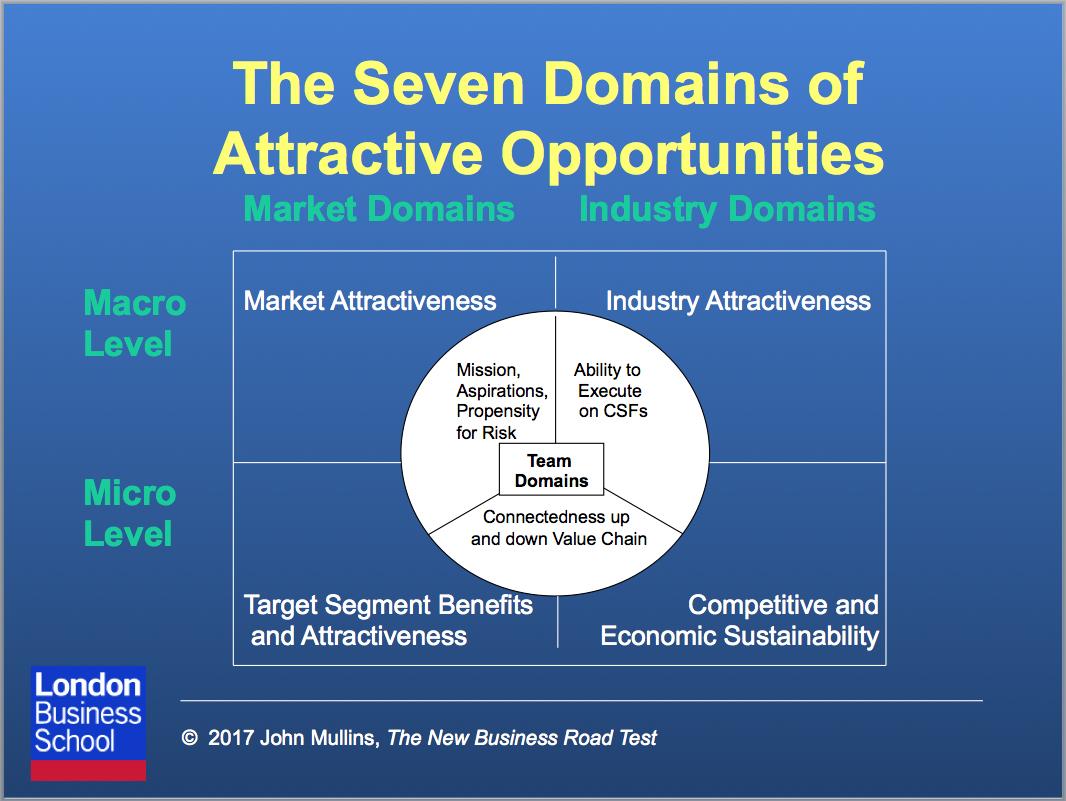

The model of Seven Domains of Attractive Opportunities introduced by John W. Mullins is an effective and powerful tool to evaluate the investment target. I recommend to use this model in combination of valuation methods for final decision making. The inner core of the model is the team domain, including its technology, strategy, execution, ability to manage cash flows and the people. I think team is one of the most important factors when evaluating investment targets, because all in all, it is all about whom we are working with, and whom we would like to make great things happen together. A combination of analysis of the target’s overall segment competitiveness, market fit and industrial attractiveness will help making better decisions.